Why a Life Cycle Assessment Beats Carbon-Only Accounting

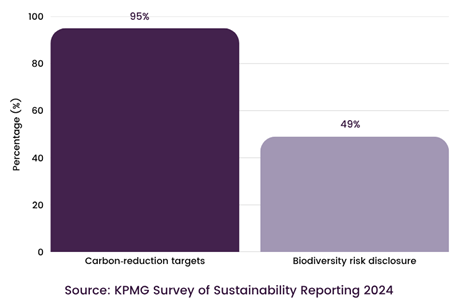

Corporate greenhouse-gas accounting took off because it is quantifiable, comparable, and increasingly mandatory. In KPMG’s 2024 global survey, 95% of G-250 firms report carbon-reduction targets, up from 80% just two years earlier. Overall, sustainability reporting is almost as widespread; however, drilling down reveals a sharp imbalance: only 49% of these companies disclose biodiversity-related risks. The result is a one-dimensional picture that obscures the impact of other materials.

Analysts have coined this imbalance “carbon tunnel vision,” warning that it limits companies’ ability to spot trade-offs and value-creation opportunities across their supply chains.

Regulations that reinforce the tunnel

Policies have certainly raised the bar for climate data, but most remain emissions-heavy and light elsewhere:

- SEC climate-disclosure rule (US): Finalised in 2024, it centres on carbon metrics and, after legal pushback, dropped any requirement to report Scope 3 (supply-chain) emissions.

- EU Corporate Sustainability Reporting Directive (CSRD) – From FY 2024, large and listed EU companies must report via ESRS under a double-materiality lens. EU regulators have deferred sector-specific standards on pollution, biodiversity, and resource use for up to two years, so carbon disclosures remain the most prescriptive element.

- State-level laws, such as California’s SB-253, likewise begin with carbon footprints before expanding to broader ecological indicators.

The net effect: Businesses receive a strong compliance signal to count their tonnes of CO₂ but only a weak nudge to quantify eutrophication potential or chemical toxicity.